ChatGPT's New Finances Feature: What It Validates, and Where It Locks You In

ChatGPT's new Finances feature just validated the talk-to-your-money thesis at 200M-user scale. Here's what it gets right, and where it locks you in.

On May 15, OpenAI added a new feature to ChatGPT called Finances. For Pro subscribers in the United States, the chatbot can now link directly to bank accounts through Plaid, the same connection layer that powers most modern personal finance apps. Once connected, ChatGPT can see balances, transactions, subscriptions, and upcoming bills, and answer questions grounded in real financial data instead of the rough estimates users normally type into the chat window. Two hundred million people, by OpenAI's own count, already ask ChatGPT about money every month. The Finances tab is OpenAI's bet that those conversations are about to become the primary way Americans interact with their money.

The bet is correct. It is also, in a way the press coverage has not quite registered, late.

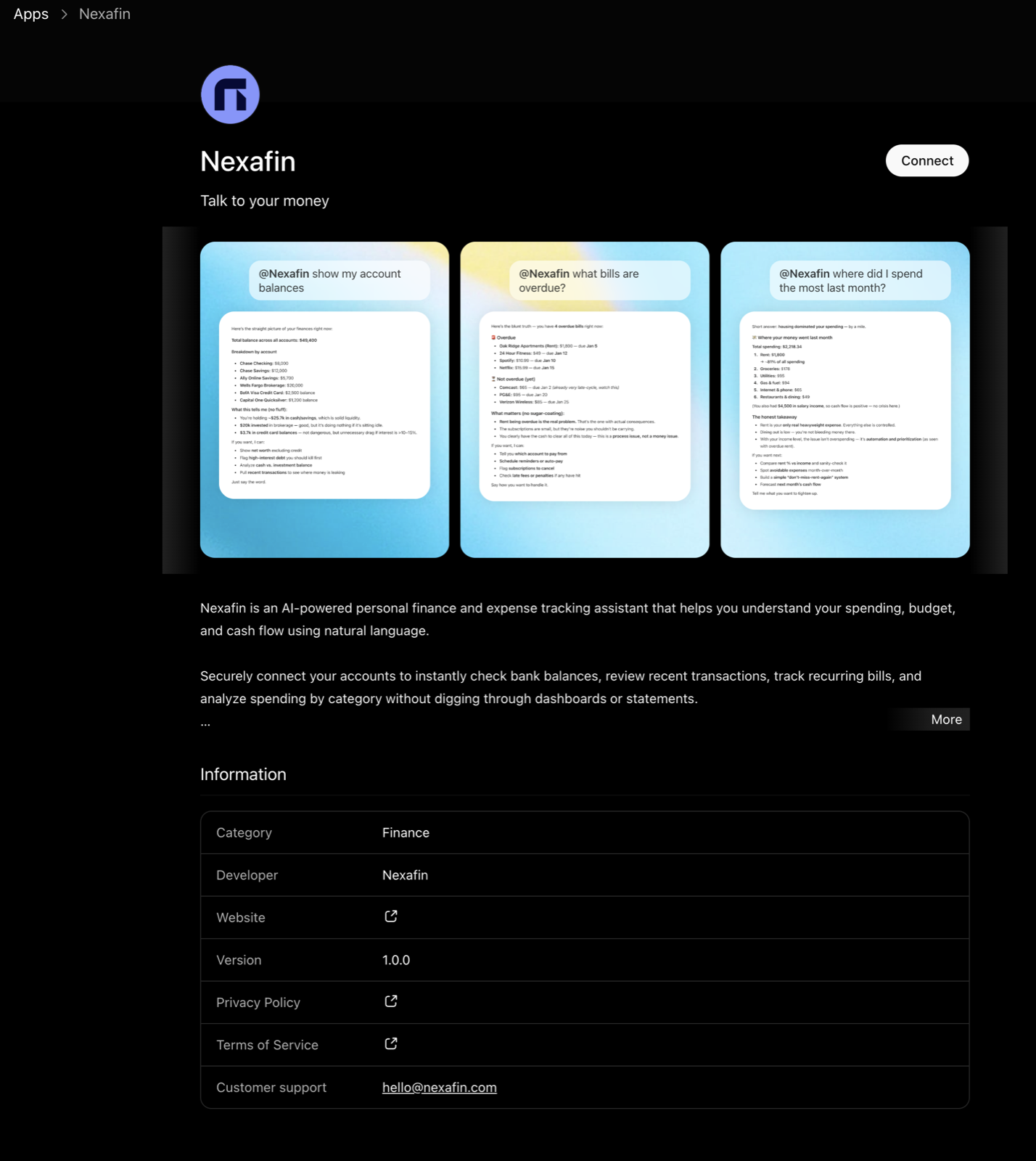

Talking to your money is not an emerging idea. It has been a shipping product for the last several months, built on top of the Model Context Protocol that lets AI assistants read real financial data without owning it. Nexafin has been operating on this premise since January, with an MCP server that connects to bank data on one end and to Claude, ChatGPT, and Claude Code on the other. The customers using it are not theoretical. The thesis has been in the field.

What is new about OpenAI's announcement is not the idea. It is the scale, and the architecture.

What ChatGPT's New Finances Feature Actually Does

The mechanics are straightforward. Users on ChatGPT Pro, the $200-per-month tier, can connect bank, credit card, and investment accounts through Plaid, which supports over 12,000 financial institutions across the United States and Canada. Access is read-only. ChatGPT can pull balances and transactions but cannot move money, change account settings, or execute trades. An Intuit partnership for tax questions and CPA consultations is on the way.

The chat is the product. "Where did last month go" produces an answer drawn from actual transactions. "Did I spend more on groceries this quarter than last" returns a real number. "Can I afford a trip to Hawaii in October" prompts a reasoning exercise that uses your real savings rate, upcoming obligations, and travel budget rather than the back-of-the-envelope figures most ChatGPT financial questions have to rely on.

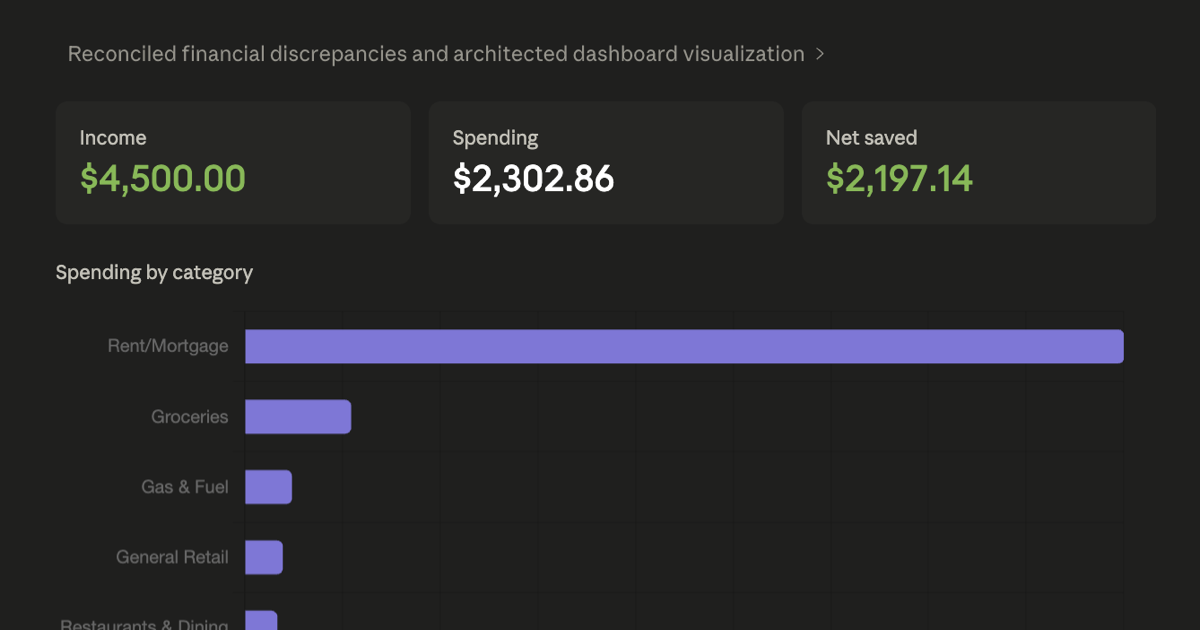

The dashboard that comes with the feature, with its lists of recurring charges and upcoming bills, is included for reassurance. It is not the part OpenAI is excited about. The conversational interface is the part OpenAI is excited about, and they are right to be.

Why Dashboards Are Becoming the Personal Finance Equivalent of the CD-ROM

For two decades, the model for consumer personal finance has been the dashboard. Mint, Monarch, YNAB, Copilot, Quicken before any of them. The interaction design was always the same: collect a user's transaction data, categorize it, render it in pie charts and line graphs, and ask the user to look at the results. The work was sifting. You scrolled through a list of charges. You dragged transactions into categories. You squinted at a spending pie chart and tried to extract meaning from the wedge labeled "Other."

The model worked, in the sense that millions of people signed up. It also failed, in the sense that almost nobody used these products for long. The retention numbers for personal finance dashboards have historically been weak, and have been for as long as the category has existed. The reason is not that people do not care about their money. It is that sifting through data is work, and the dashboard format offloads the work onto the user.

Conversational interfaces invert the relationship. Instead of building the dashboard and asking the user to extract meaning from it, the AI does the extraction and hands back an answer. "Why was March more expensive than February" gets a sentence, not a chart. "Which subscription is most likely one I forgot about" gets a recommendation, not a list to scroll through. The cognitive work that dashboards used to offload to the user moves to the model.

This is the actual significance of the ChatGPT launch. OpenAI has not invented a new category. They have confirmed, at the scale of two hundred million monthly users, that the dashboard is no longer the center of the experience. Personal finance is becoming a conversation. The argument worth having is not whether the transition is happening. It is who owns the conversation.

ChatGPT Validates the Thesis. Then Locks the Door.

OpenAI's Finances feature is built around the assumption that the conversation will happen inside ChatGPT, and only inside ChatGPT.

The connection to your bank lives there. The categorizations live there. The patterns the model learns about your spending live there. The goals you mention in passing, the recommendations the model has made, the conversation history itself, all accumulate inside OpenAI's product. The data is technically portable. OpenAI says synced data is deleted within thirty days of disconnection. But the entire system is built around the assumption that you will never disconnect.

If, eight months from now, Claude becomes better than ChatGPT at reasoning over a year of transactions, you cannot point Claude at the financial context you have been building up. If a new model arrives next year that beats them both, you start from scratch. Whatever AI assistant ends up being best at understanding your money, it has to be ChatGPT, because that is where your money's history lives.

This is not a technical limitation. It is the business model. OpenAI is not interested in being one of several AI assistants you talk to your money through. They are interested in being the only one.

The Real Limits of ChatGPT's Bank Connection

Four constraints will determine how widely OpenAI's version of "talk to your money" actually gets used.

Price. Finances requires ChatGPT Pro at $200 a month, or $2,400 a year. Plus subscribers, who pay $20 a month and make up the overwhelming majority of paying users, are not in the rollout. The minimum cost of asking AI about your finances through OpenAI's official channel is one of the most expensive consumer software subscriptions on the market.

Geography. The preview is United States only. Anyone banking in Canada, the United Kingdom, the European Union, or anywhere else is excluded. There is no announced international timeline.

One AI. Your financial context is accessible to ChatGPT and to no other model. Not Claude, not a domain-specific assistant, not whatever ships next year. You can only ask the chatbot that owns the connection.

One Vendor. OpenAI is now the company that holds the relationship between you and your bank data. If their pricing changes, if their model regresses, if their policies shift, your finances move with them. There is no separation between the AI provider and the data layer underneath.

The Open Version of Talk to Your Money

The opposite architecture is the one Nexafin has been shipping since January.

The data layer lives in the finance app. Bank connections, transactions, subscription detection, and bill tracking all run on Nexafin's infrastructure. AI access happens through a read-only MCP server, which is approved for the ChatGPT App Store and also connects to Claude and Claude Code. The same financial data is available through whichever AI a user prefers. Claude today. ChatGPT today. Whatever model is best six months from now.

The geographic coverage is wider as well. Plaid handles US and Canadian banks. GoCardless covers the United Kingdom and the European Union. CSV and PDF imports work for users whose bank is in neither network. Pricing is $9.99 a month or $79.99 a year, which is roughly four percent of the ChatGPT Pro tier you would otherwise need.

The architectural difference is the entire pitch. ChatGPT's Finances binds the AI and the data into one product. Nexafin separates them. The AI is a guest in your finance application, not the landlord.

What This Announcement Actually Means

Two hundred million money questions a month is not a niche. It is a demographic. OpenAI's Finances feature confirms what a handful of companies, Nexafin among them, have been building toward for the last several months: the next phase of consumer personal finance is conversational, and the dashboard era is closing.

The confirmation is useful. The category has arrived. The argument now is about its shape.

OpenAI's shape is closed and centralized. One AI assistant, one country at launch, one chat window, one company holding the relationship to your bank. The alternative shape is open and federated. The data lives in a finance application that any AI can read through MCP. The AI you talk to is your choice, today and next year.

The question is not whether you should talk to your money. ChatGPT just settled that one. The question is whether you have to talk to it through ChatGPT.

Ready to take control of your finances?

Track spending, monitor net worth, and gain clarity on your money.

Start Free Trial →